Prices Climb and Listings Shrink - San Francisco Market Update

June 19, 2025

June 19, 2025

Quick Take

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

Click here to JUMP TO NATIONAL DATA

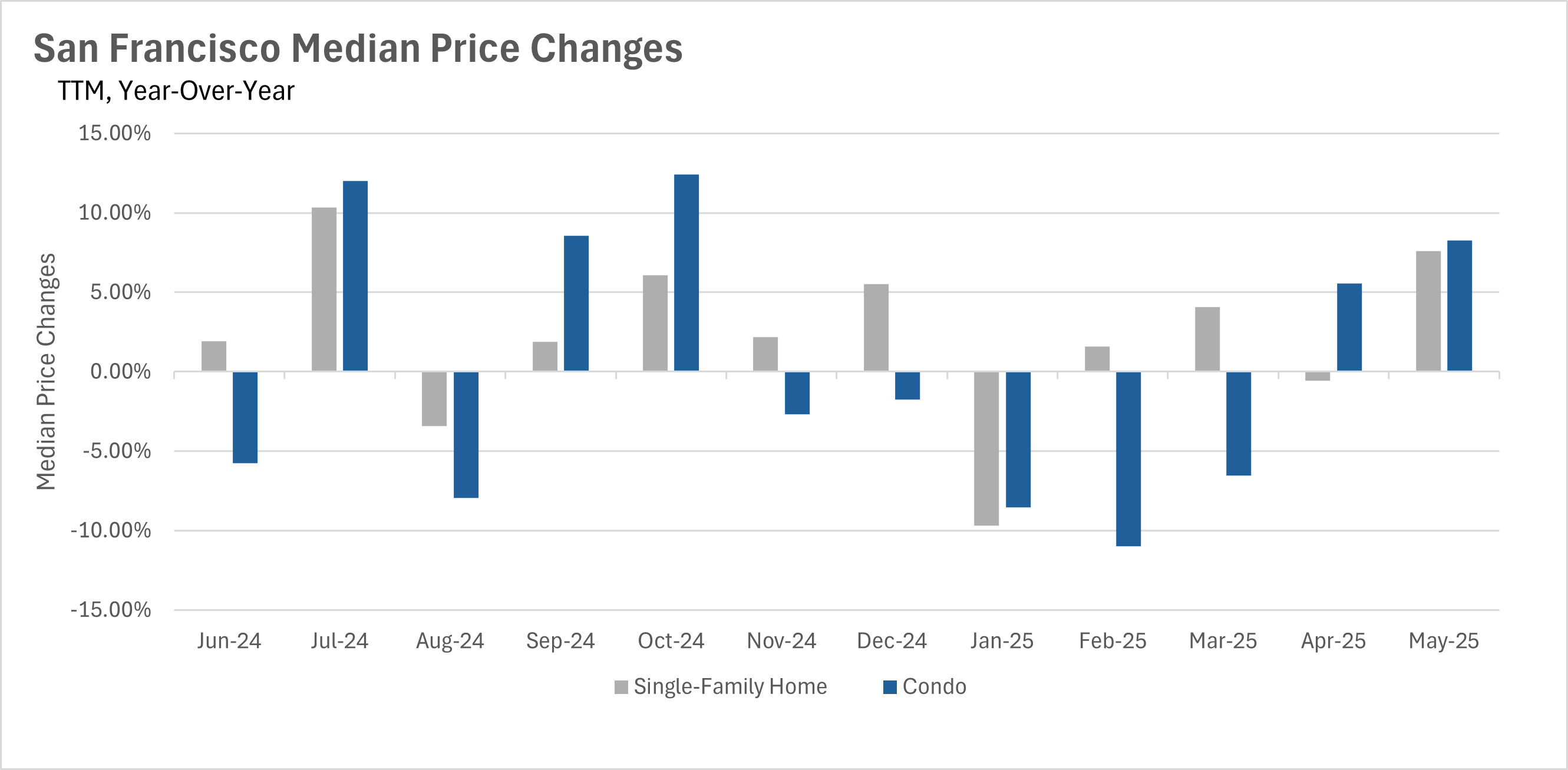

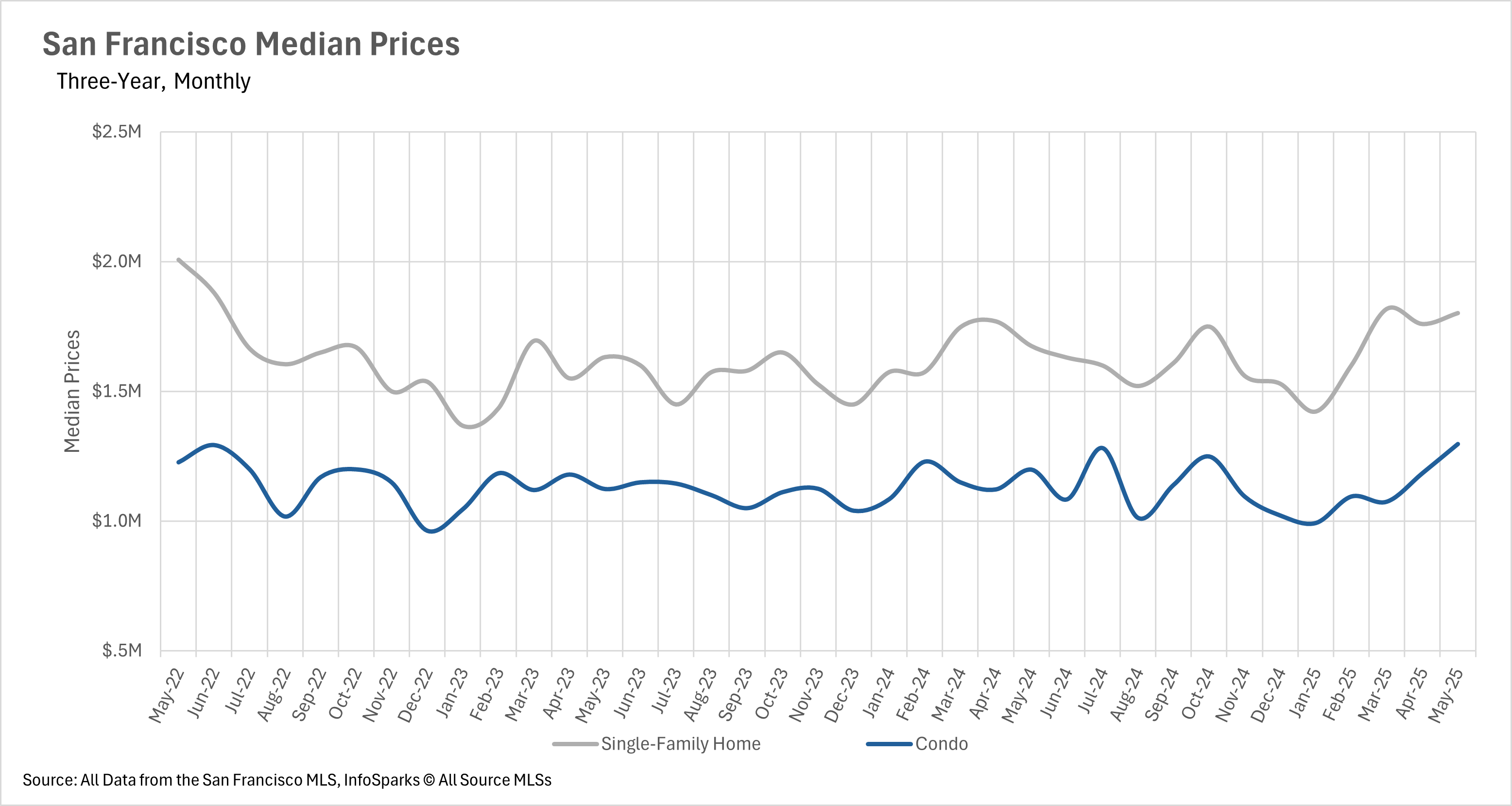

Although many markets have seen a downtrend in pricing, San Francisco has remained incredibly resilient. In fact, in the month of May, we saw quite a surge in median sales prices, with home values reaching some of the highest levels we’ve seen in over two years. The median single-family home was sold for $1,802,000, a 7.58% increase compared to May of last year. Whereas the median condo was sold for $1,298,000, representing a year-over-year increase of 8.26%. This phenomenon is likely due to the fact that inventories have been downtrending for years at this point.

As we just mentioned, inventories have been on the downtrend in San Francisco for years, and this streak continued in the month of May. Single-family home inventories were down 2.54% on a year-over-year basis, despite the fact that they were up 5.49% on a month-over-month basis. This phenomenon is interesting, as sales were down 7.39%, while new listings were up 8.72% on a year-over-year basis.

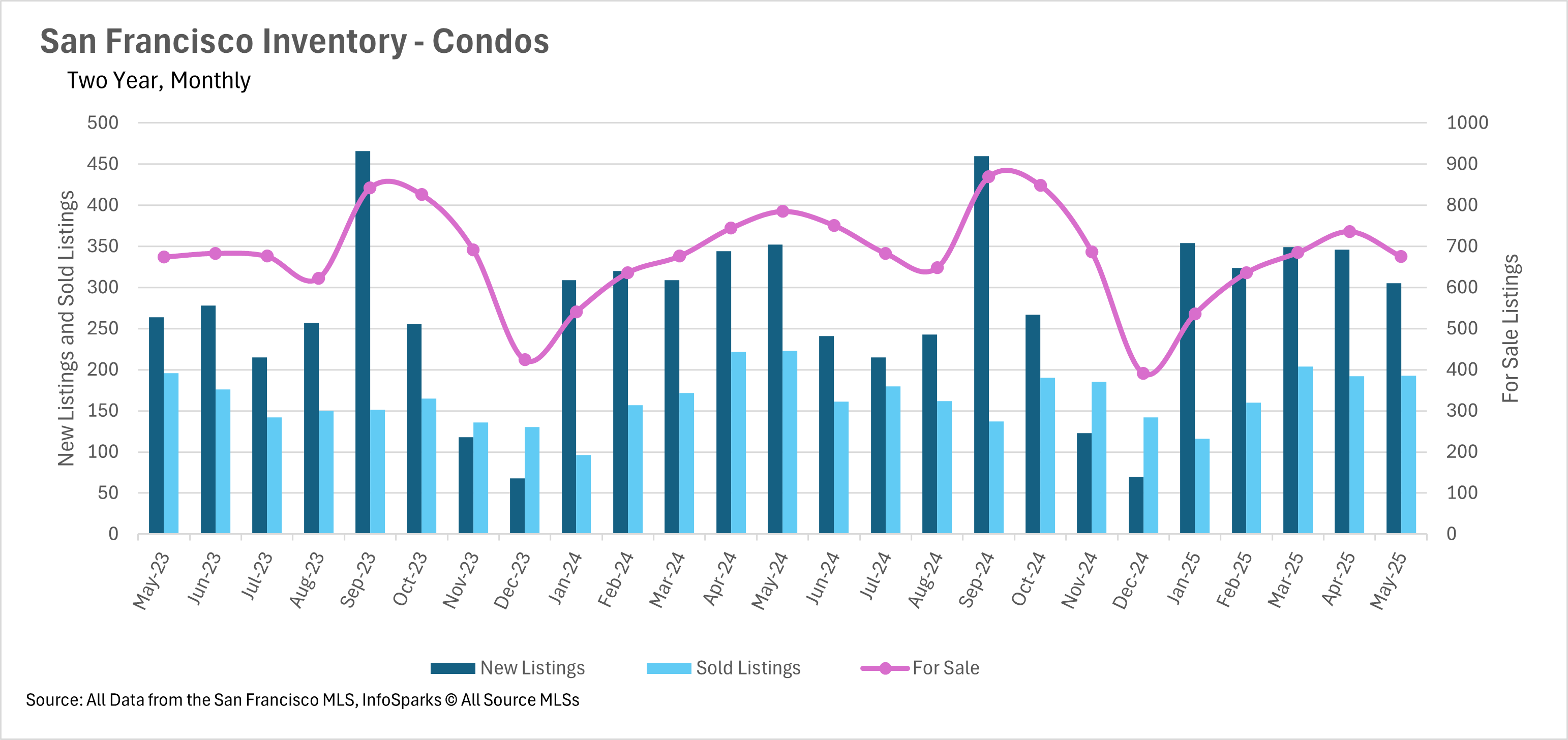

When we turn to the condo market, we see an even more drastic decline, with there being 14.01% fewer active condo listings than this time last year. This drop in inventory falls roughly in line with the 13.35% decrease in new listings and the 13.45% decrease in sold listings on a year-over-year basis.

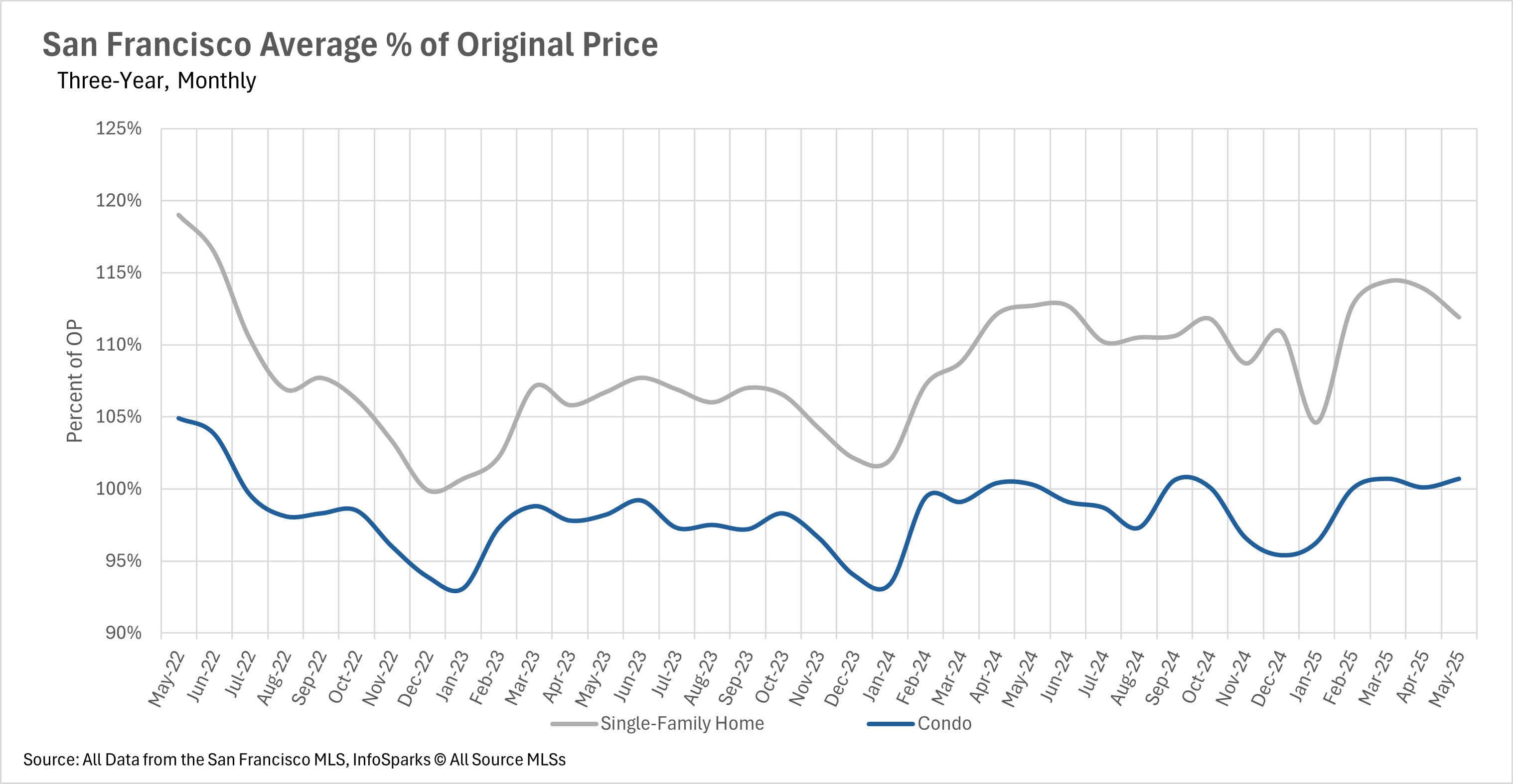

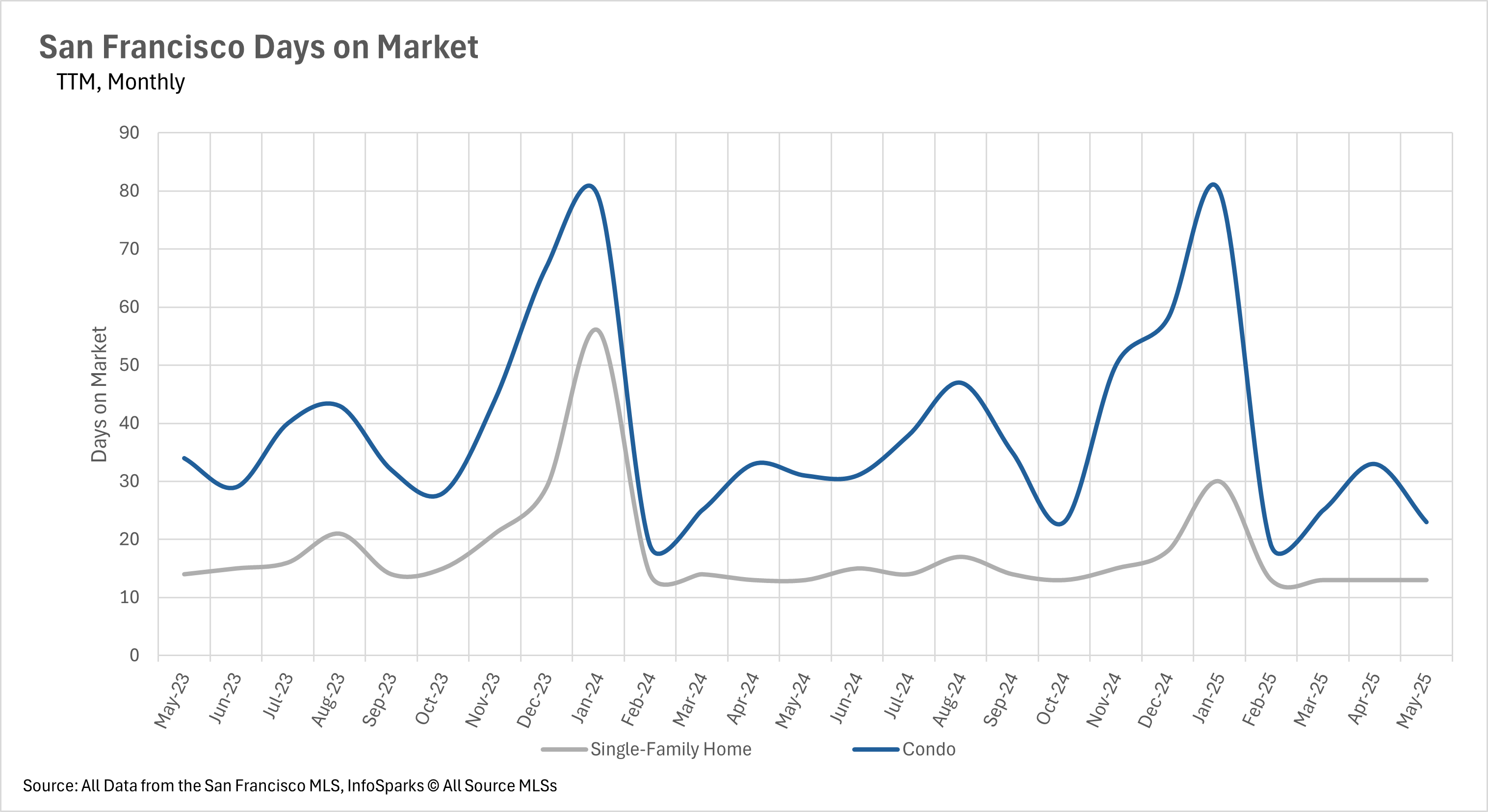

Since inventories have been trending lower, it’s probably not surprising to hear that listings are selling very quickly in San Francisco. The average single-family home lasts just 13 days on the market, which is exactly how long it took for a listing to sell around this time last year. Condos do take a bit longer to sell though, with the average condo sitting on the market for 23 days before it sells. This is still relatively fast, and this figure represents a 25.81% decrease from the 31 days on the market we saw last May!

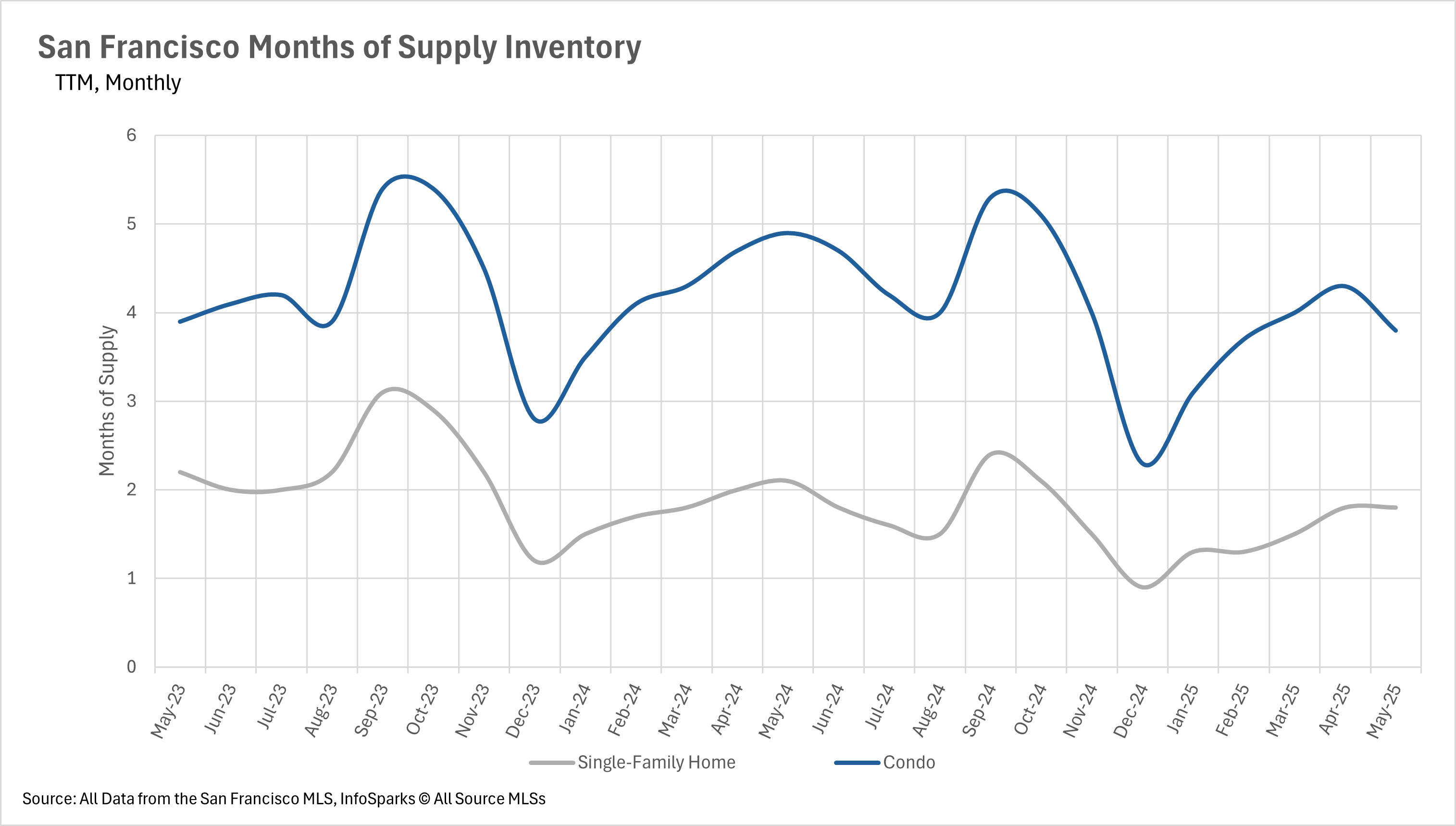

When determining whether a market is a buyers’ market or a sellers’ market, we look to the Months of Supply Inventory (MSI) metric. The state of California has historically averaged around three months of MSI, so any area with at or around three months of MSI is considered a balanced market. Any market that has lower than three months of MSI is considered a sellers’ market, whereas markets with more than three months of MSI are considered buyers’ markets.

In San Francisco, the single-family home market has been a sellers’ market and the condo market has been a buyers’ market for quite some time. Although this month is no different, we did see some year-over-year declines in the number of months of supply on the market. The single-family home supply declined by 14.29% to 1.8 months worth of inventory, and the condo market declined by 22.45% to 3.8 months of inventory.

Quick Take:

Note: You can find the charts & graphs for the Big Story at the end of the following section.*National Association of REALTORS® data is released two months behind, so we estimate the most recent month's data when possible and appropriate.

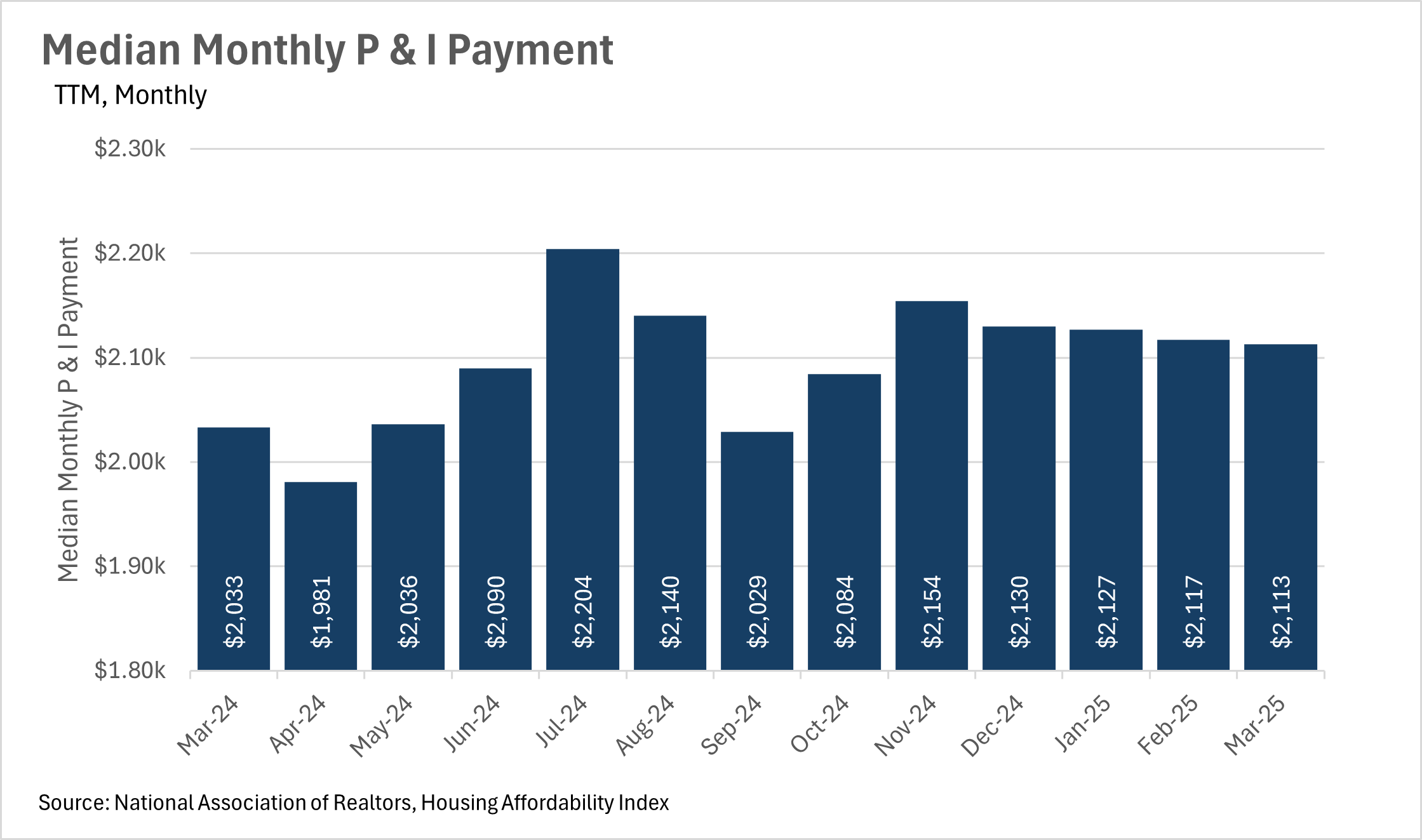

For quite some time, we’ve seen monthly inflation readouts with figures in the 2-3% range. Despite the fact that inflation seems to be under wraps for now, the median monthly P&I payment has grown faster than inflation, with the most reading coming in at $2,113, representing a 3.94% increase on a year-over-year basis. This shows that there are still inflationary pressures at work in the housing market.

Factors contributing to this inflation will vary by market. Some markets have more of an issue on the supply side (i.e. higher construction/materials costs), while others have an issue with the demand side (i.e. more demand for homes than supply). It will be especially important to pay attention to this metric over the coming months to get a gauge of how inflation is impacting the housing market.

Mortgage rates have remained high, in the mid to high-6% range for quite some time. Some believe that the recent trade war was being implemented in part to bring down interest rates. However, judging by recent commentary from the Fed, the trade war and the associated uncertainty, has only made Fed officials more cautious in utilizing the incredibly powerful economic tool that is the federal funds rate.

This means that we are probably going to see elevated mortgage rates for the foreseeable future, unless the economy takes a considerable turn for the worse. It is worth noting though, that according to the Fed’s “Dot Plot”, the majority of Federal Reserve officials predict the federal funds rate will be in the 3.75-4.00% range by the end of the year, and the 3.25-3.50% range in 2026.

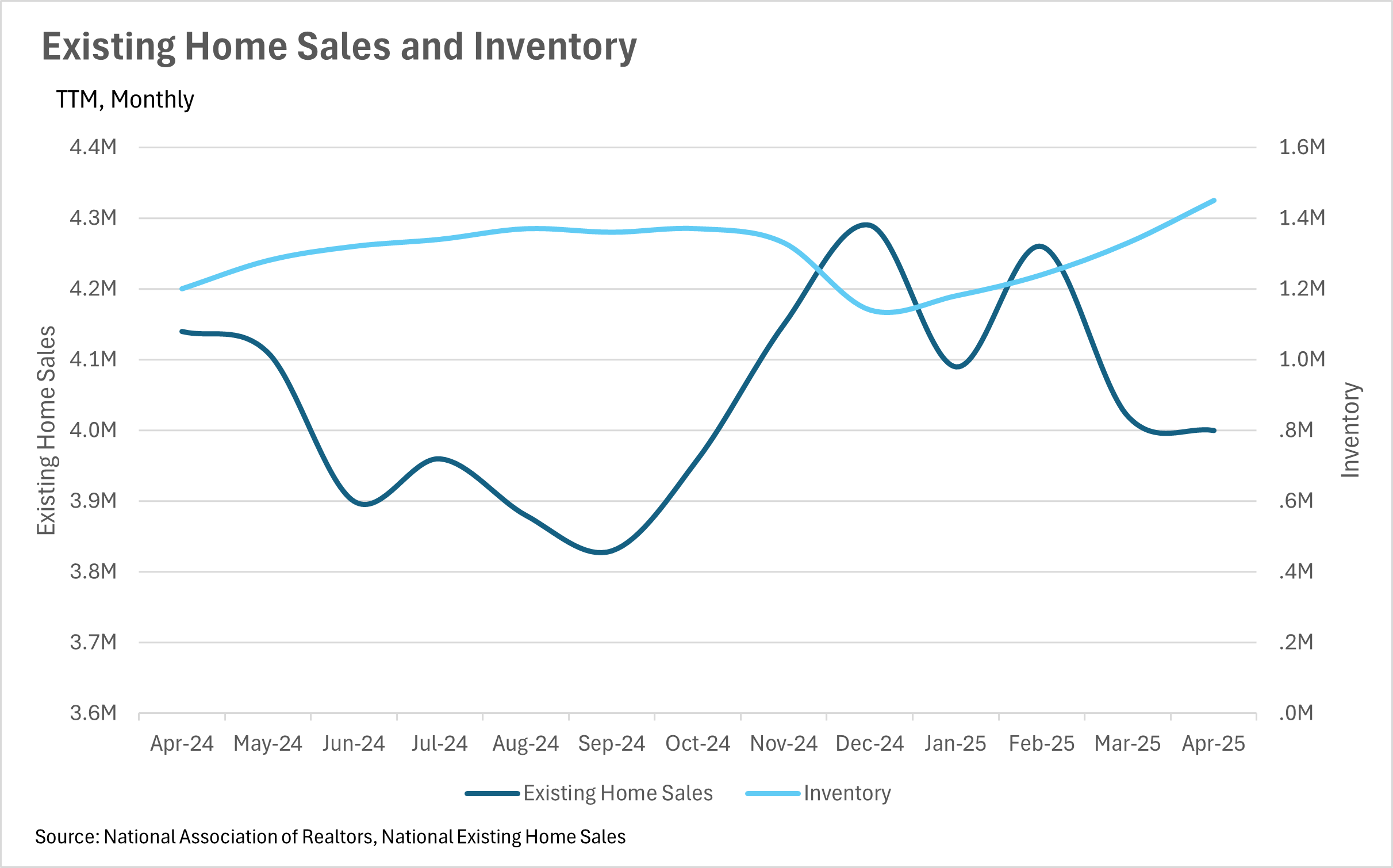

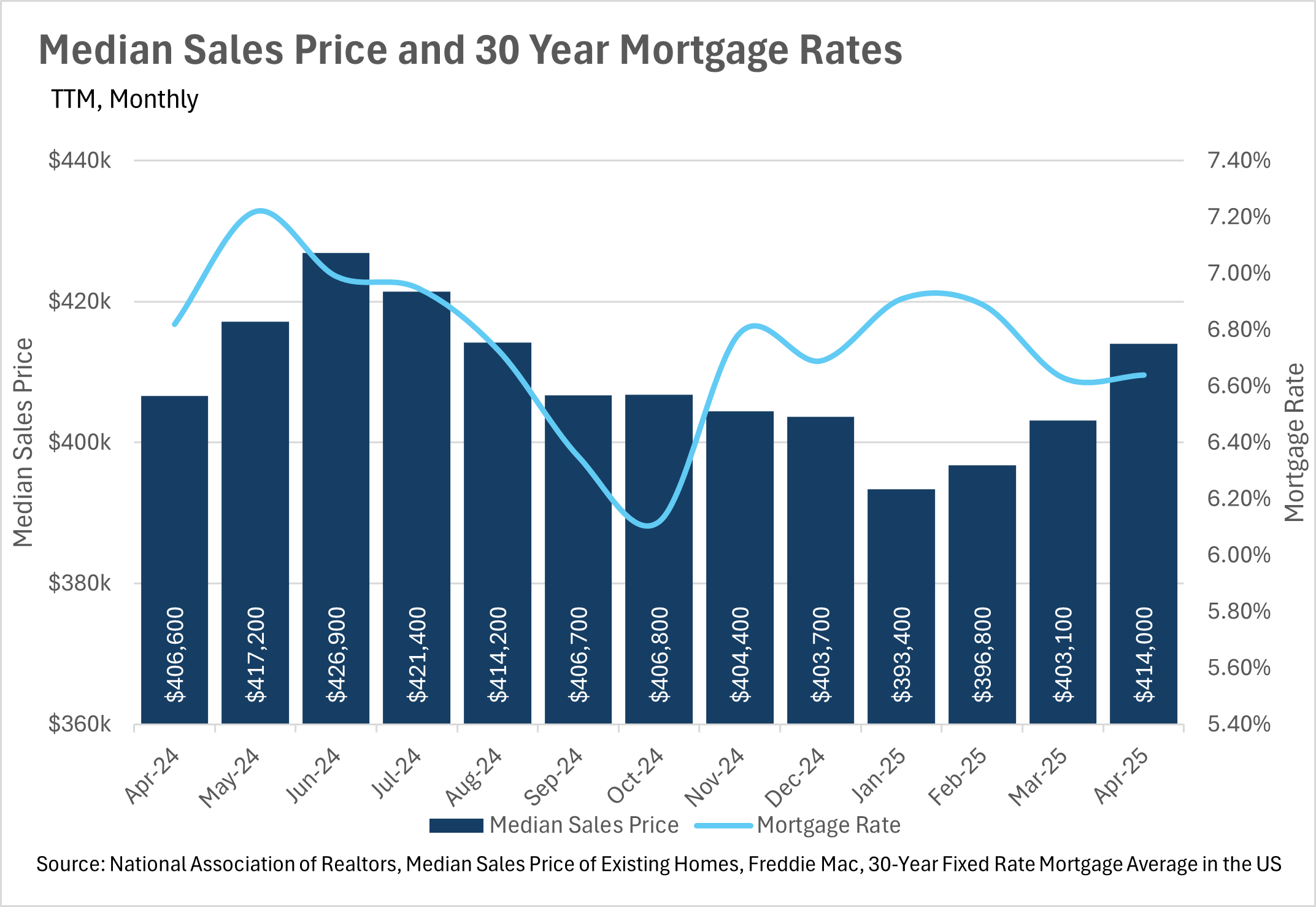

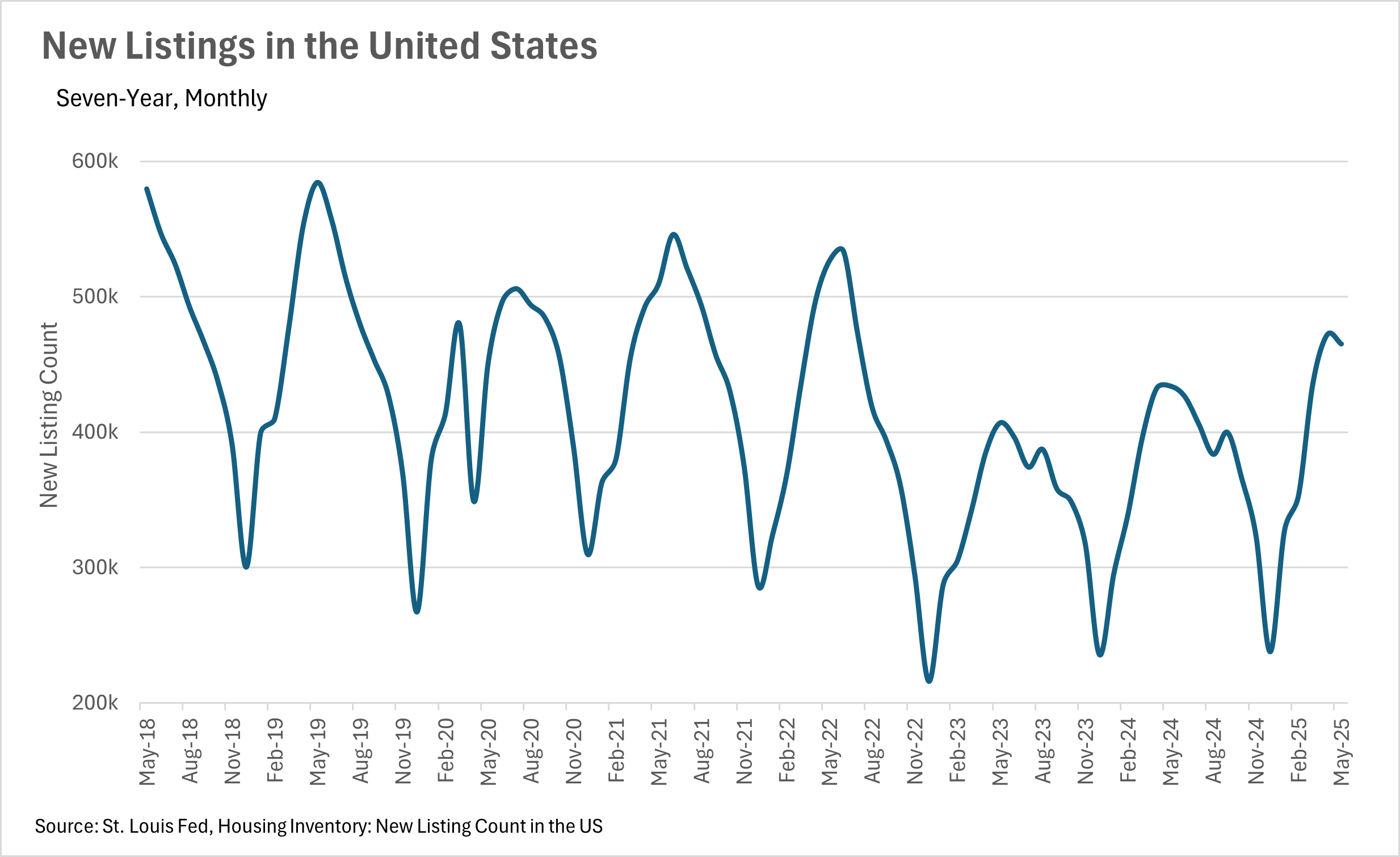

The moves in sales and inventory that we’ve been seeing throughout California over the past few months have been echoed on a national scale. The nation as a whole has seen inventories build, as homes sit on the market for longer. Our most recent data point (April 2025), shows that inventory increased by 20.83% on a year-over-year basis, to 1,450,000. Meanwhile, existing home sales decreased by 3.38%, to 4,000,000.

Despite the growing backlog of inventory, median sale prices are still trending upward, with the median listing selling for $414,000, representing a 1.82% year-over-year increase. To add fuel to the fire, we’ve seen growing numbers of listings hitting the market, with the number of new listings hitting the market increasing by 7.19% on a year-over-year basis.

Ultimately though, this is just what we’re seeing at a national level. As we all know, real estate is an incredibly localized industry, so knowing what’s going on in your own market is pivotal. Below is our local lowdown, that outlines everything you need to know about what’s happening around you in your neighborhood and surrounding areas!

Stay up to date on the latest real estate trends.

July 24, 2026

June 2026 market data shows record-low inventory, rising home prices, and one of California's strongest seller's markets.

July 23, 2026

More than 140 San Francisco homes sold over $1 million above asking in early 2026.

July 17, 2026

Explore Life Near the Panhandle at 536 Broderick

July 14, 2026

June 2026 Pacifica housing market data, including median sale price, days on market, price per square foot, and sale-to-list price trends.

You’ve got questions and we can’t wait to answer them.