September Analysis – where did all the housing go?

September 26, 2019

September 26, 2019

Each month we analyze the nuances of the San Francisco housing market and for insight into the latest market changes, you have come to the right place! This monthly snapshot of San Francisco Bay Area real estate helps us guide our buyers and sellers to make decisions based on the most up-to-date market data and we are happy to share this insight with you. KEEP READING BELOW.

If you know anyone living in Bernal or Baview or has expressed interest in moving there.

SIGN THEM UP for exclusive access to our neighborhood market analysis.

|

|

This Month’s Local Inventory Market Data

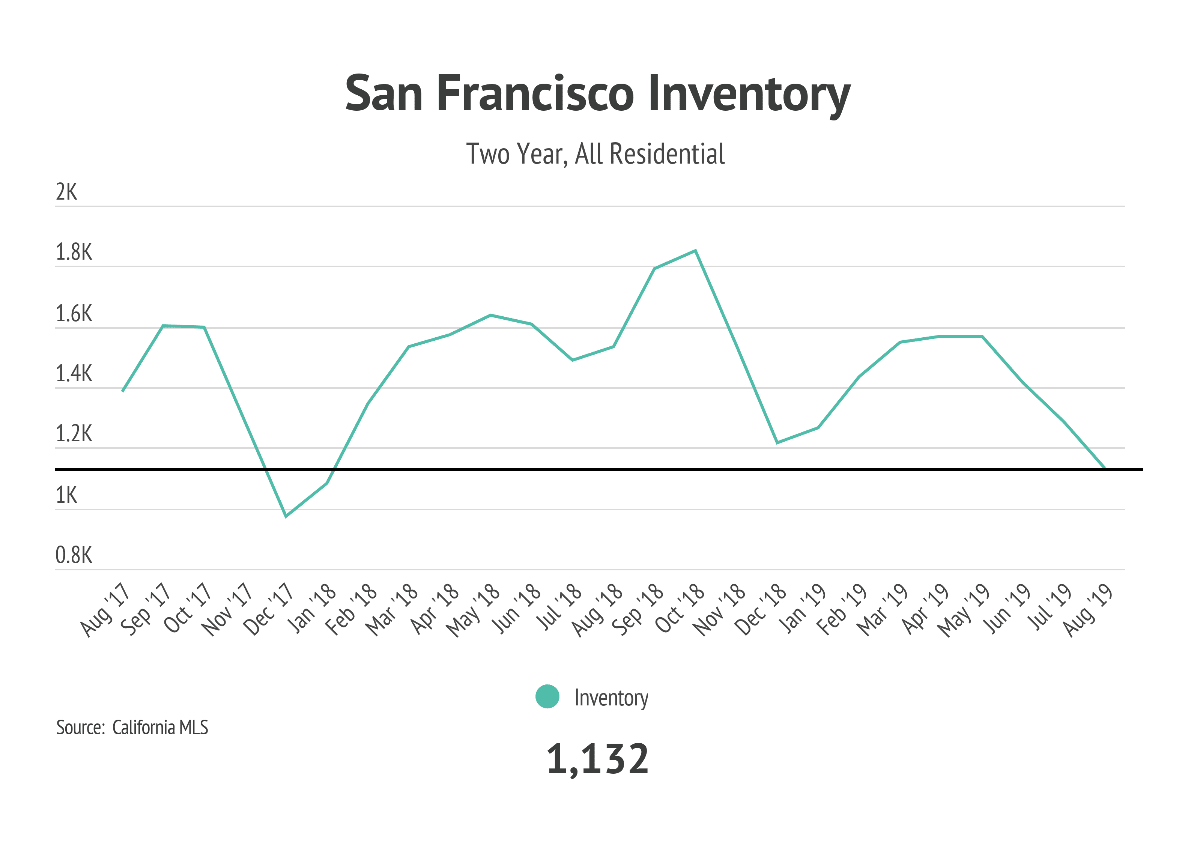

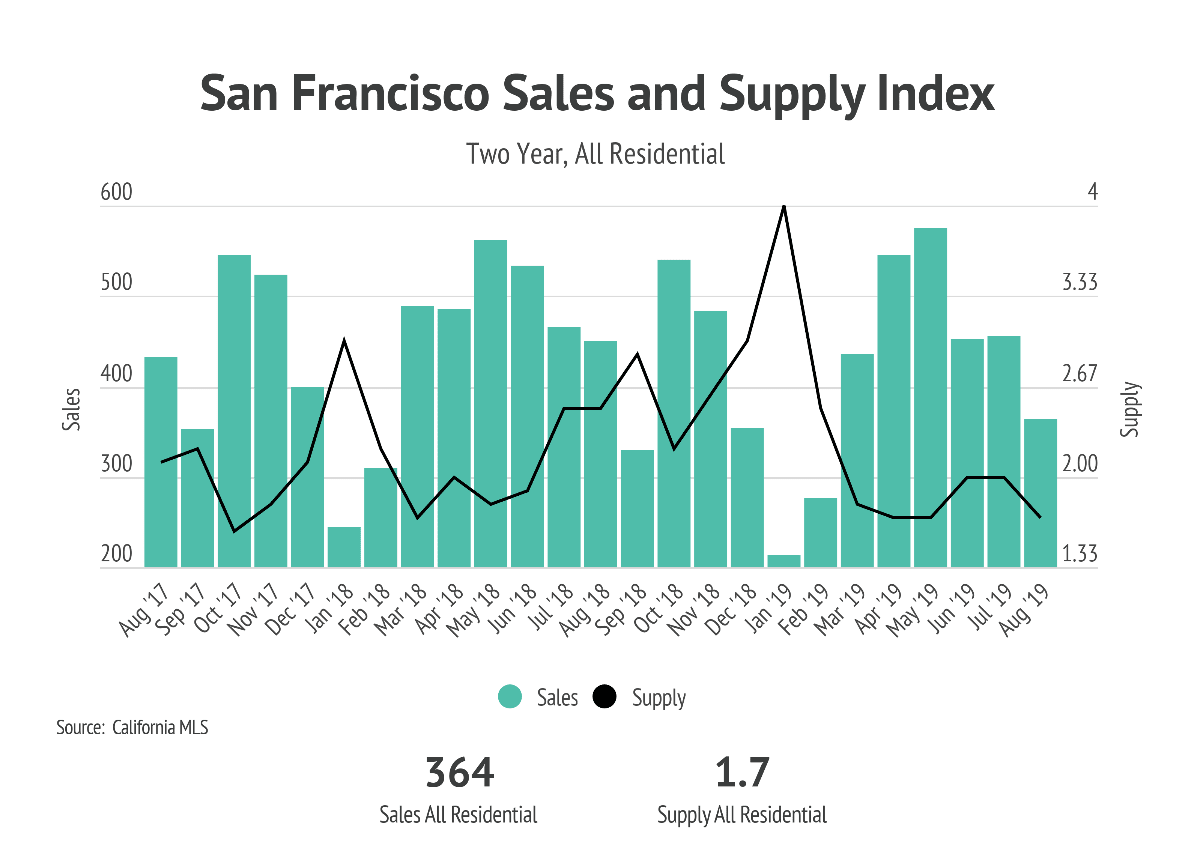

San Francisco’s shifting housing inventory continues to drive prices in the city. Although inventory rose during the first half of the year, August’s residential inventory is significantly lower than it was this time last year.

The chart above shows San Francisco’s inventory levels from August 2017 to August 2019. The waterline indicates that the last time inventory levels were this low was during the winter of 2017/18 when seasonal inventory drops are typical.

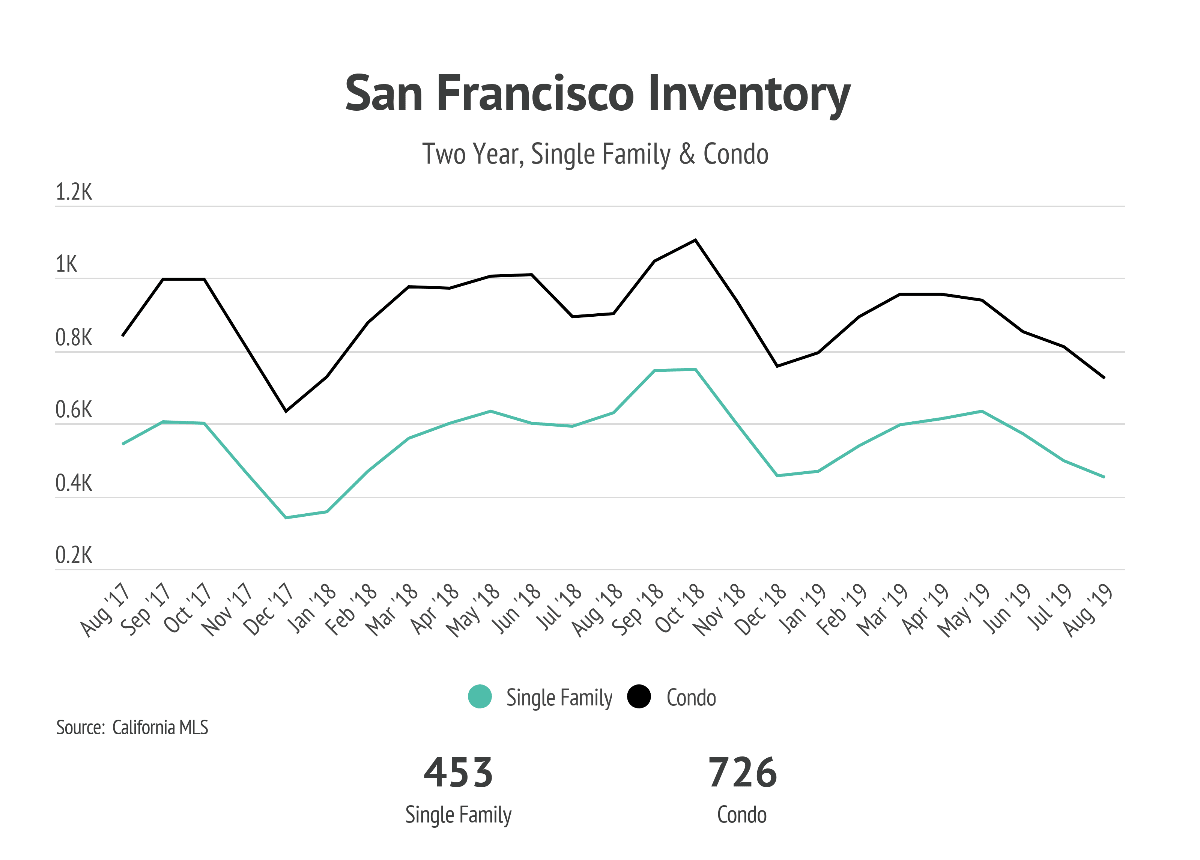

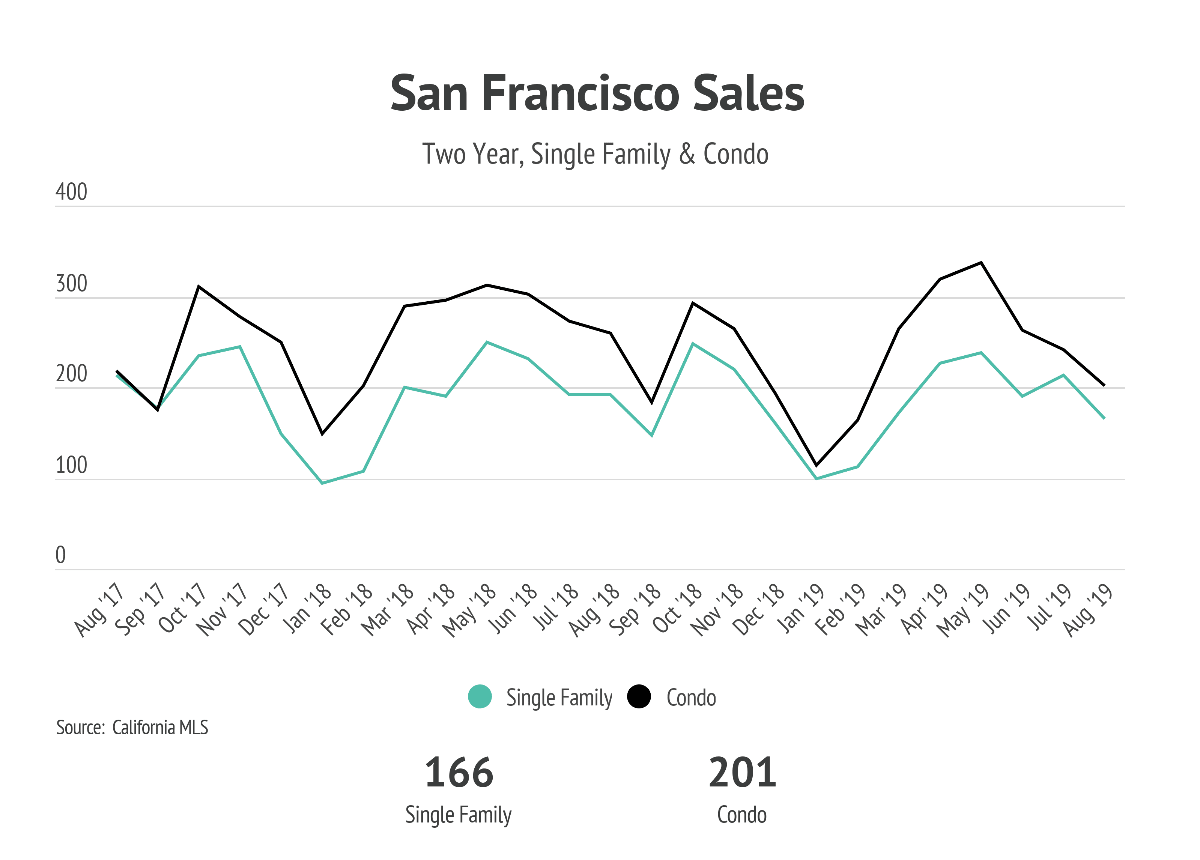

If we look at the past 12 months (August 2018-2019) compared to the previous year (August 2017-2018) in the chart below, we can see that inventory has been falling steadily for both single-family homes and condos.

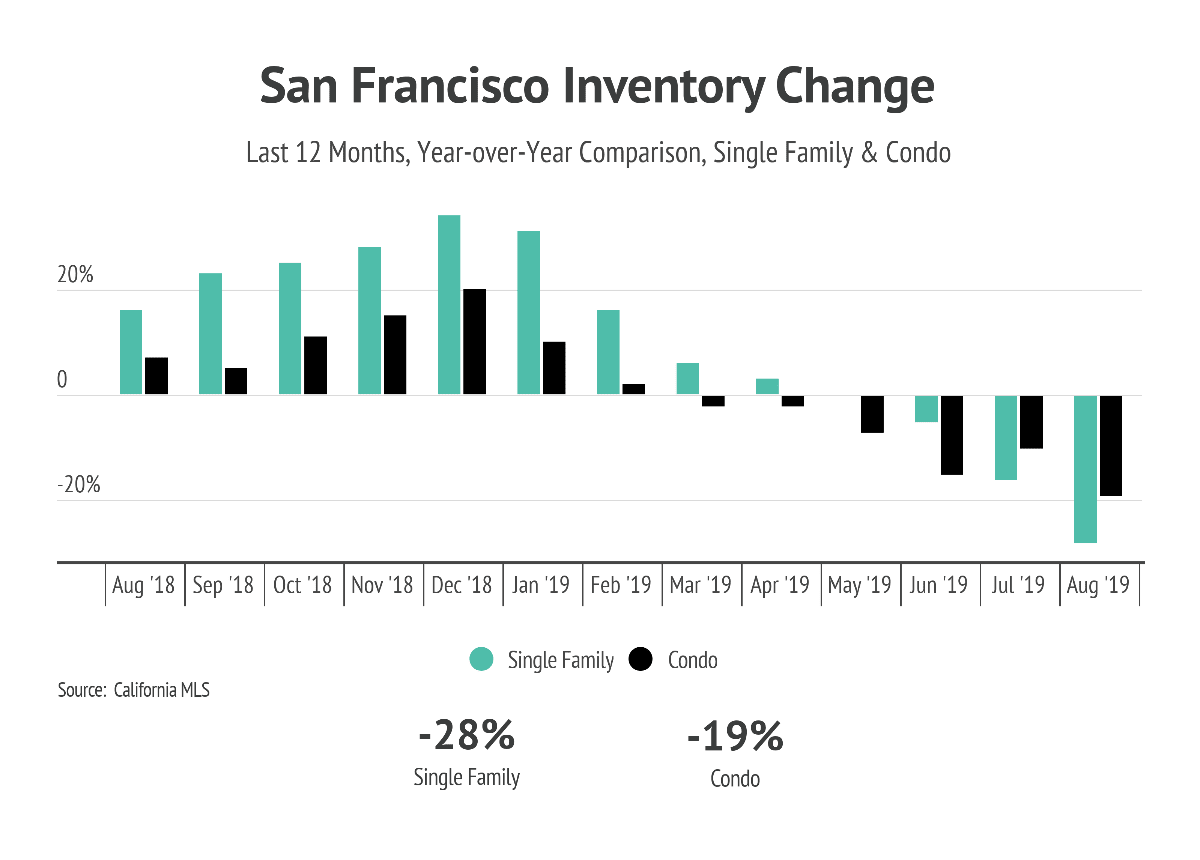

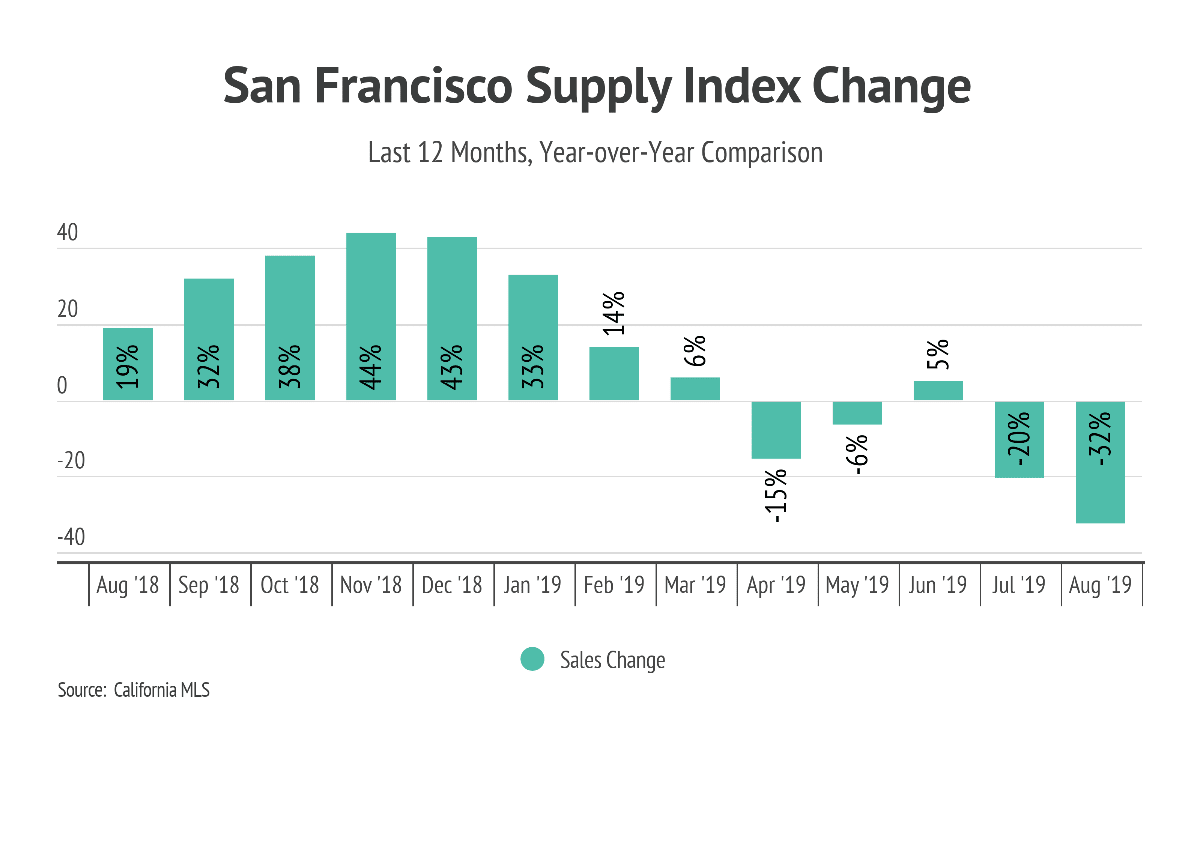

Inventory increased last year when interest rates began to rise. However, interest rates fell during the spring months, which took any excess inventory off the market.

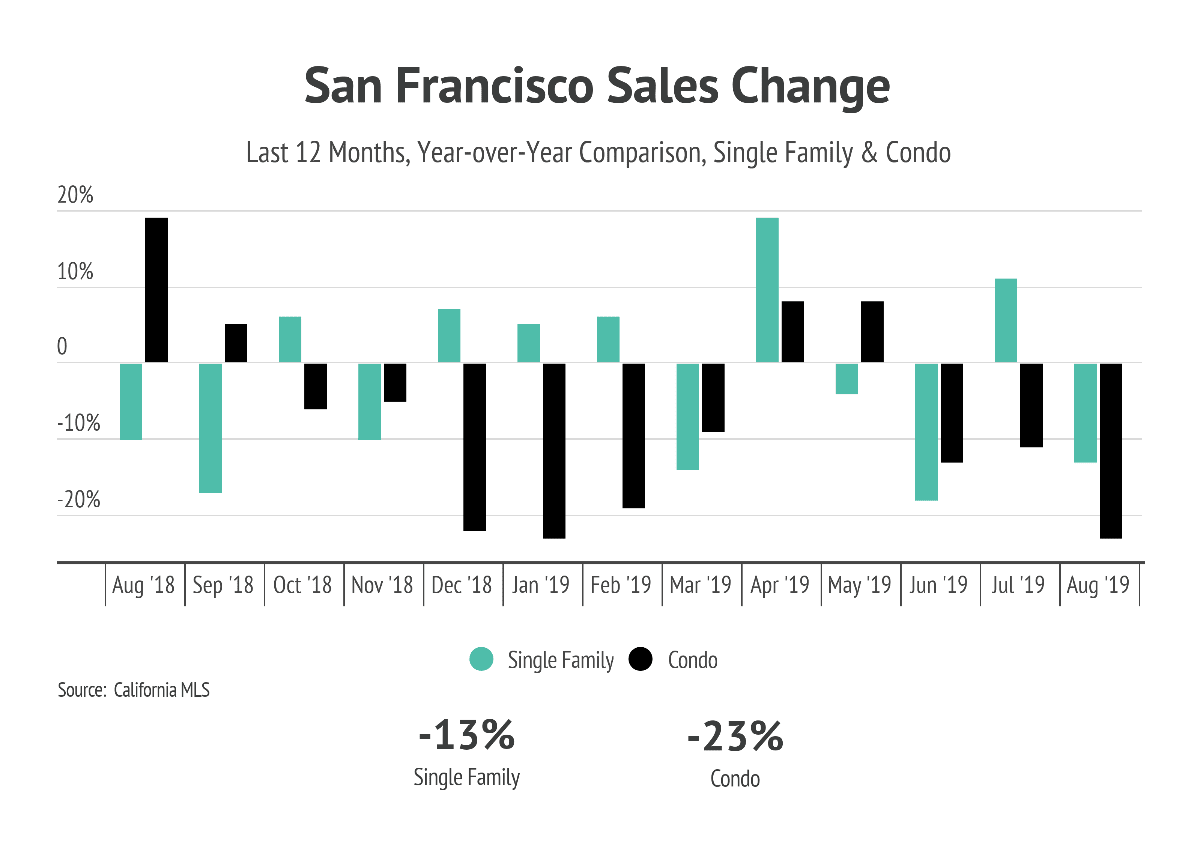

In August 2019, however, sales for both single-family homes and condos were down compared to the previous year. For example, there were almost 600 more homes on the market in August 2018 than there were one year later.

Weak sales typically indicate soft demand, which reduces median home prices. However, the current lack of inventory is keeping the overall supply index low—lower, in fact, than this time last year.

This combination of factors is propping up prices. In the month of August, the median price of all residential properties (which include single-family homes and condominiums) rose on a year-over-year basis by 2% to $1,400,000.

Analysts, such as those at the National Association of Realtors, believe low housing could be related to the tax code changes that took place at the beginning of 2018. The NAR writes:

As a result of the changes made throughout the legislative process, NAR is now projecting slower growth in home prices of 1-3% in 2019 as low inventories continue to spur price gains.

It is here that we can take a closer look.

The Impact of Tax Code Changes on Housing Inventory

In December 2017, Congress passed the Tax Cuts and Jobs Act, which took effect on January 1, 2018. The government implemented a standard deduction granting taxpayers a base tax write-off of $12,200 for single households or $24,400 for married households.

The law has little impact on homeowners in areas where home prices are below $750,000 and households with smaller itemized deductions, such as state, local, and property taxes. For homeowners in pricier areas, however, the new tax law is noteworthy—especially for those with homes worth $1 million or more.

The graphic below shows us what that impact might be.

Our assessment is that the new tax code burden is not large enough to significantly impact home affordability or buying and selling patterns. To further understand this conclusion, we look at price segments most affected by the inventory change.

|

|

|

|

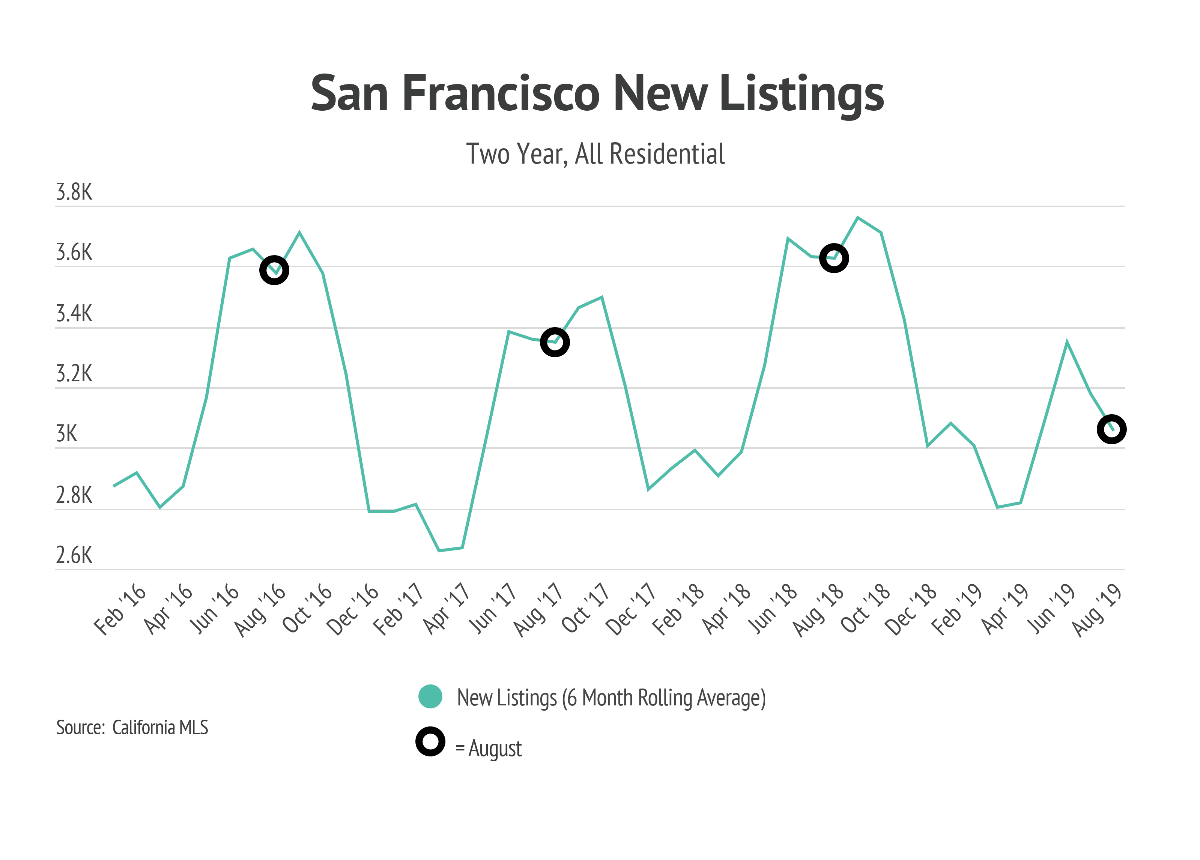

The chart above tracks the number of new listings in August for the last four years and shows a steep drop in listings this year.

The chart above tracks the number of new listings in August for the last four years and shows a steep drop in listings this year.

Low Housing Inventory: The Impact on Buyers and Sellers

Low housing inventory impacts both buyers and sellers.

For buyers, low inventory means less choice, which means finding a home may be difficult. In August 2019, the sold price of the median home was 10% over the list price. Today’s buyers need to be prepared to act fast and make an offer above list price.

For sellers, the tight market might seem like an opportunity to command any price. However, median home prices have failed to push through the current high watermark of $1.7 million.

Homes without price reductions sold for 10% above their original list prices, but homes with one or more price reductions sold two or three points below. The bottom line? Pricing a home to sell is more of a science than an art.

|

|

|

Stay up to date on the latest real estate trends.

March 26, 2026

Smart Strategies to Overcome Buyer Struggles in 2026

March 25, 2026

Home prices jumped sharply in February as inventory stayed extremely tight and buyers moved quickly across both single-family homes and condos.

March 10, 2026

A Hidden Opportunity for Homebuyers in the San Francisco Housing Market

March 6, 2026

Explore Bayview Businesses and Amenities (Map)

You’ve got questions and we can’t wait to answer them.