The Big Story

No Default!

Quick Take:

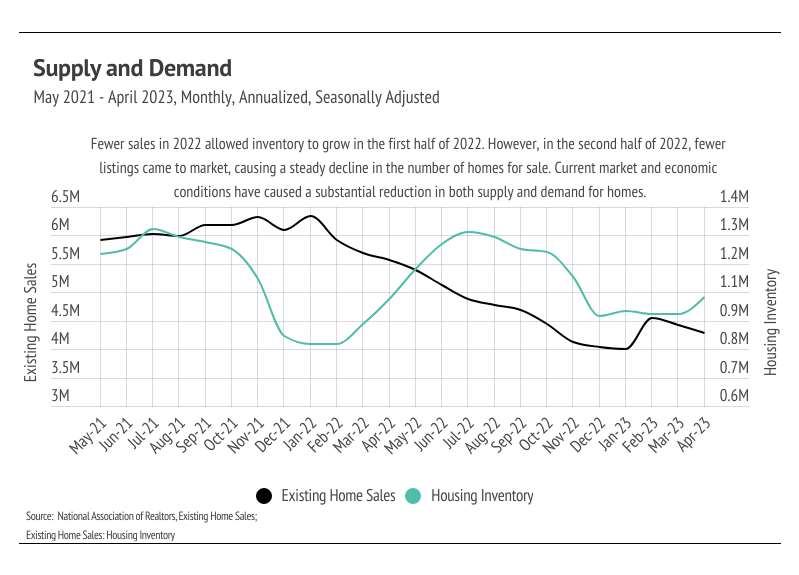

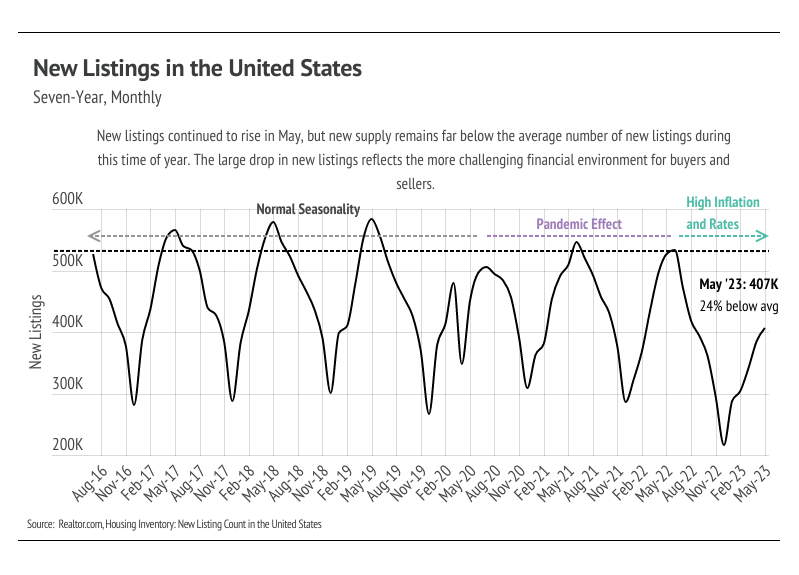

- Home sales fell 3.4% month over month as homebuyers faced volatile mortgage rates and sustained low inventory. Far fewer new listings have come to market this year and, in May, new listings were 24% below the long-term average.

- The United States narrowly avoided a catastrophic and self-inflicted credit default, allowing the Fed to focus on the robust labor market and generally strong economy in an effort to decide whether to continue hiking rates.

- Broadly, home prices have contracted slightly from the peak they reached in June 2022, but the steady rate increases have slowed down the housing market significantly, even compared to the years before the white-hot market of 2020-2022.

Note: You can find the charts & graphs for the Big Story at the end of the following section.

The labor market is too strong for a recession, so what’s the Fed to do?

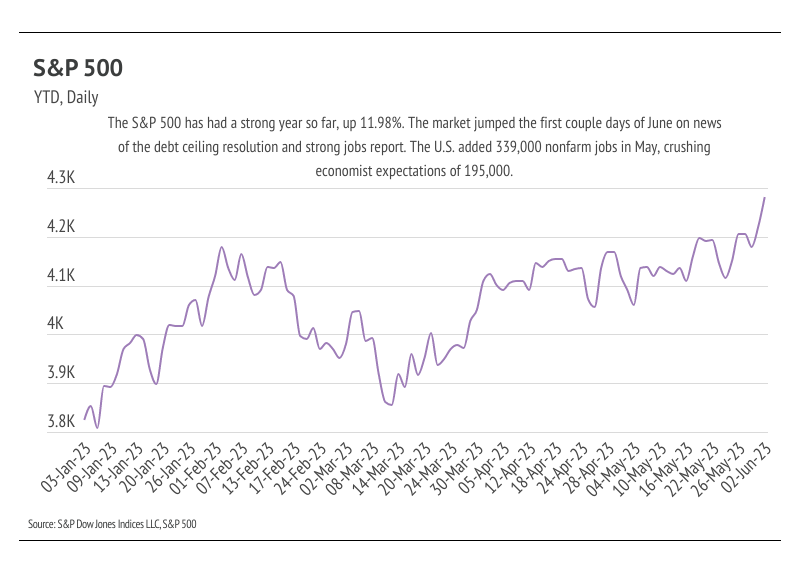

We did it, gang! We made it through another debt ceiling crisis! The United States paid its bills in full and on time, avoiding default and a global economic catastrophe with two days to spare. This self-inflicted wound would have had far-reaching negative economic consequences in the near and long term, including far higher mortgage rates. Financial markets were mostly unbothered despite the fact that this Congress seems to be the most amenable to default. The 10-year Treasury yield rose a modest 0.4% in May, which translated to a 0.4% increase in the average 30-year mortgage rate. The S&P 500, which tracks the stock of the 500 largest publicly traded U.S. companies, reached a high for the year at the beginning of June, up 12% year to date. To be fair, a debt ceiling resolution that didn’t totally destroy the U.S.’s global standing was the most probable scenario. Now that the debt ceiling has been lifted until 2025, we turn our sights back to the Fed and interest rates.

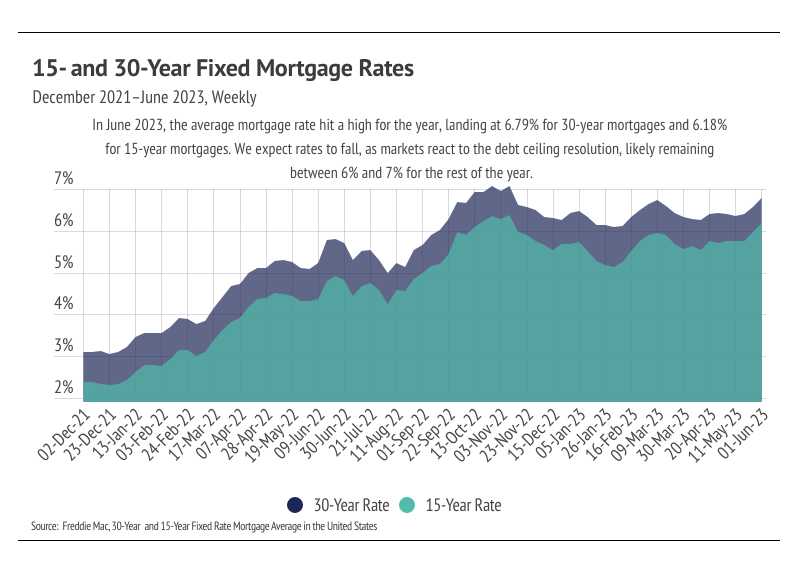

During their last meeting, the Fed forecasted a potential pause in rate hikes after three sizable regional bank failures this year, but recent jobs data may swing them back toward a 0.25% increase. Increasing mortgage rates have primarily driven the housing market slowdown we’ve experienced over the past 12 months. Higher rates affect the housing market so strongly because housing is typically financed. Potential buyers have struggled with mortgage rate volatility over the past 18 months, as the average 30-year mortgage rate went from historic lows in 2021 (~3%) to a 20-year high (~7%) in November 2022. Luckily, rates contracted but have remained around 6.5%. Because home prices nationally haven’t contracted substantially from their all-time highs, small rate changes can make a huge difference in the cost of financing. The average 30-year rate hit a 2023 high at the start of June. However, we still expect rates to stay within the 6-7% band this year. At this point, continued rate hikes tell us more about the length of time rates will stay high, since the Fed tends to move in smaller steps over time. This means that, for every step up, there will need to be a step down, which will prolong the process of returning to lower mortgage rates.

The Fed has a tricky decision regarding future rate hikes. The broad labor market has shown its strength and seeming immunity to rate hikes. The monthly increase in employment from the U.S. Bureau and Labor Statistics has beat Wall Street estimates for the 14th month in a row. In May alone, 339,000 jobs were created, crushing the expected 195,000 jobs. At the same time, however, unemployment rose from 3.4% to 3.7% from April to May. Additionally, the first-quarter 2023 GDP data was revised up from 1.1% to 1.3% quarter over quarter. With this mix of data, we’re expecting a rate hike pause at the June meeting, but a hike again in July.

The housing market is in an interesting spot, where the economy is too good to lower rates but homes have become too expensive for potential buyers. Fewer sellers and buyers are in the market, so sales are unlikely to grow meaningfully this year.

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. In general, higher-priced regions (the West and Northeast) have been hit harder by mortgage rate hikes than less expensive markets (the South and Midwest) because of the absolute dollar cost of the rate hikes and the limited ability to build new homes. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Big Story Data