The Local Lowdown: Winter buying opportunities

December 14, 2022

December 14, 2022

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

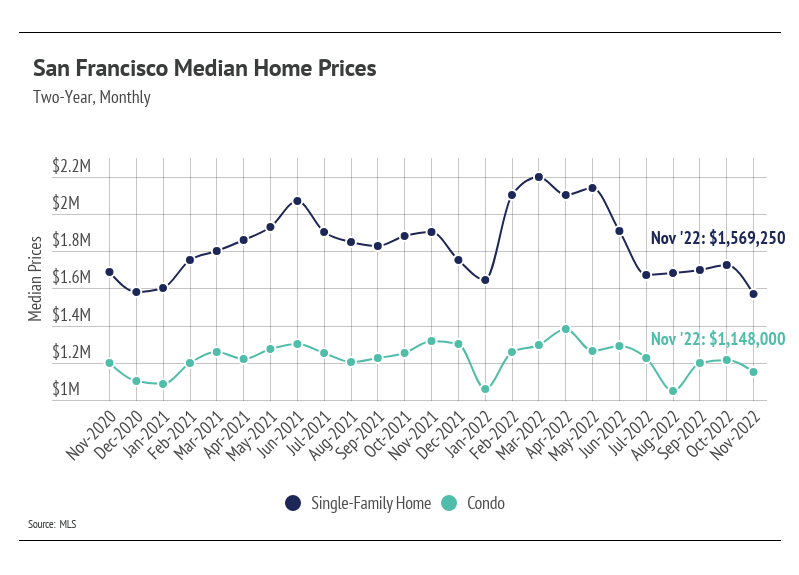

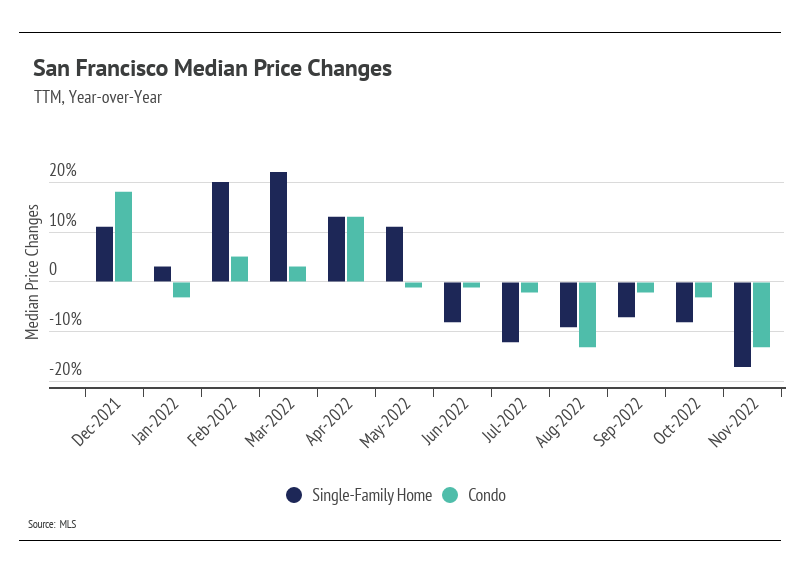

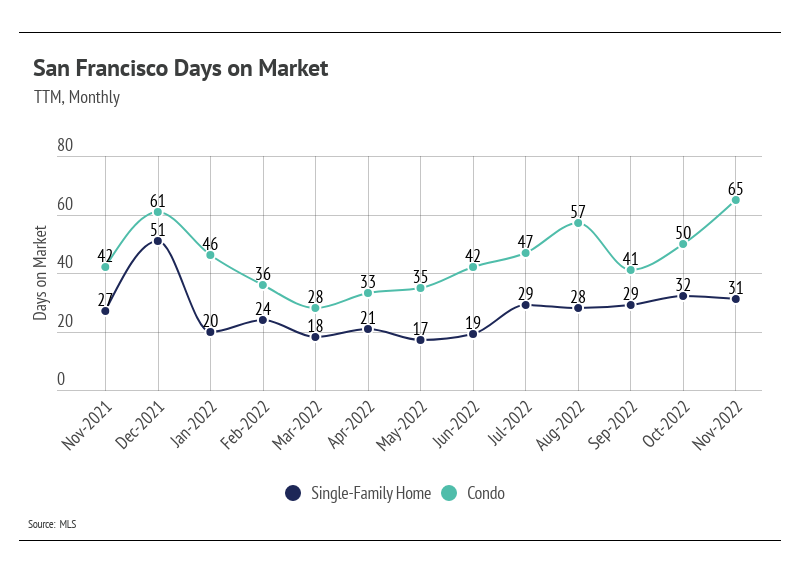

The San Francisco market is cooling on both the buy and the sell sides. When there are fewer sellers, there are also fewer buyers, because some buyers are selling their homes to move to others in the same market. New listings have declined faster than sales, causing inventory to decline near the historically low level we experienced last winter. However, the key difference is that fewer buyers are on the market — so, even with low inventory, buyers can still find the home that’s right for them. The low inventory has insulated prices from a major reversal. Single-family home prices have declined 29% from the March peak, which matches remarkably well with the increasing cost of a loan due to the rate increases. Not that you would or could finance the whole cost of the $2.2 million median home at 3.5% in March, but the cost of a $2.2 million mortgage at 3.5% is essentially the same as the cost of November’s $1.56 million median-priced home at 6.5%. Condo prices haven’t declined as significantly as single-family homes, down 17% from the April peak.

Moving forward, prices will likely contract slightly more through the winter, which is typical. Without any signs of interest rates dropping, we’re entering a stage of slower, longer-term growth — but still growth. In the short term, however, prices may come down a little more. Real estate has shown itself to be one of the best investments in recent history and is, on average, the largest store of wealth for an individual or family. Price appreciation will likely move to a more normal growth rate of around 5-6% in the coming years, which makes for a much healthier market than what occurred in 2020 and 2021.

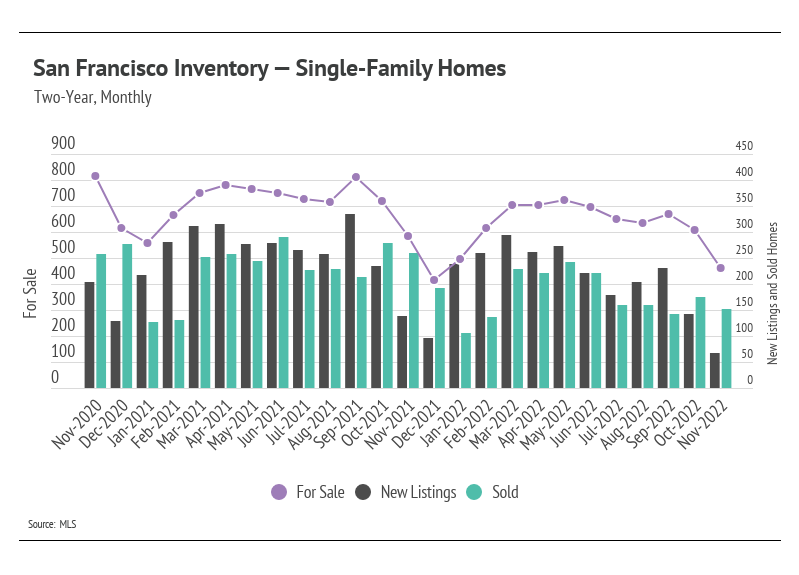

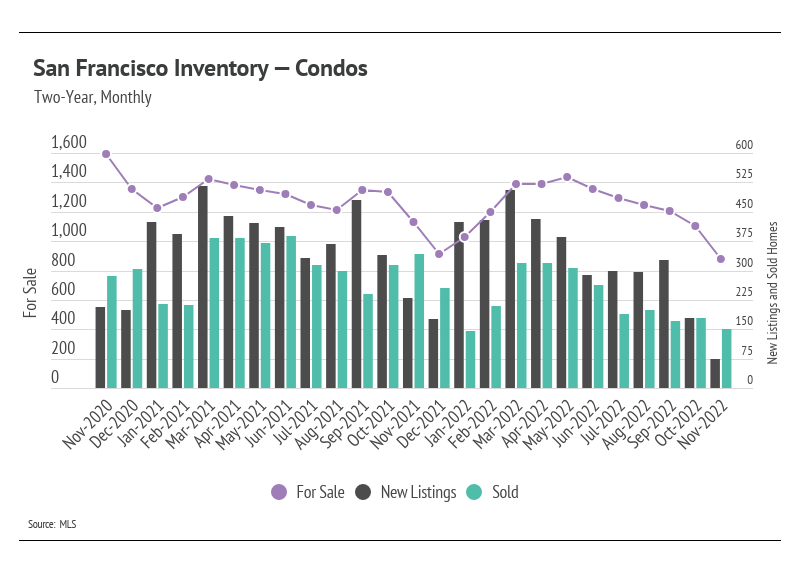

San Francisco, along with the rest of the country, has not returned to anywhere near pre-pandemic inventory levels after the buying boom last year. Inventory in 2022 failed to accumulate meaningfully throughout this year. We can compare sales and new listings from 2021 to 2022 to see the effects of fewer homes coming to market. Fewer homes and the rising rate environment have dropped demand. Softening demand has brought the market back to a sellers’ market for single-family homes and toward balance for condos despite declining inventory.

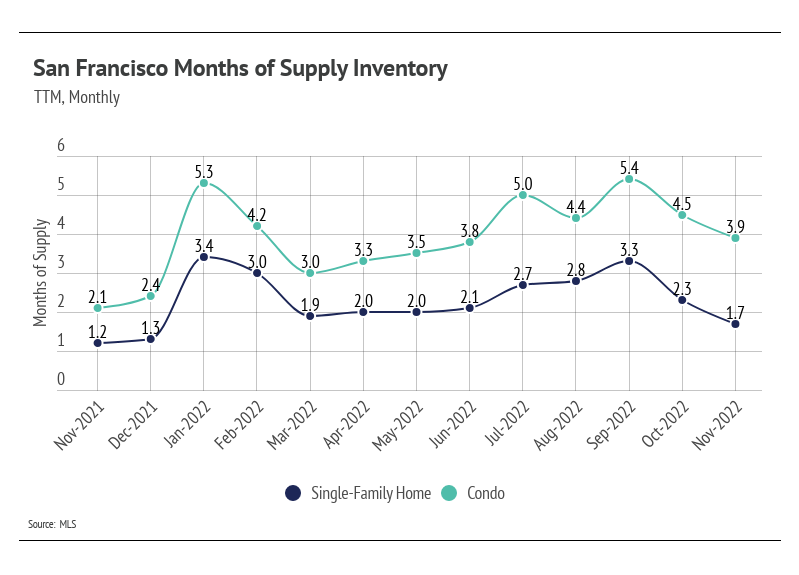

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI trended higher (away from a sellers’ market) in the spring and summer before inventory began to decline due to steady sales and a drop in new listings. The lack of inventory for single-family homes and condos has driven MSI lower, indicating the market favors sellers for single-family homes and is near balance for condos.

Stay up to date on the latest real estate trends.

May 28, 2025

Know Your Budget, Understand Your Limitations

May 22, 2025

DALP provides eligible homebuyers with up to $500,000 in down payment assistance

May 19, 2025

National & Local Housing Market Update

May 14, 2025

Discover the Silver Terrace neighborhood—a sunny, diverse community offering spacious homes, local parks, and unbeatable commuter access for families and professionals… Read more

You’ve got questions and we can’t wait to answer them.